PART 7 — FINANCIAL STRUCTURES & BANKING CHANNELS: Q1 2026 GLOBAL COMMODITY MARKETS

WEALDRAED THRYMMELLEN

Email: info@wealdraedthrymmellen.org

Phone: +971 58 540 3888

Downloadable link: https://drive.google.com/uc?export=download&id=16huleqgxU2FkY8RIyn-J50JVIdUAXGvs

Report Period: January – April 2026

Published: May 2026

Sources: S&P Global Platts · Argus Media · LME · CBOT · Baltic Exchange · EIA · IEA · USDA · World Bank · LBMA · OPEC · FAO · ISCC · wealdraedthrymmellen.org

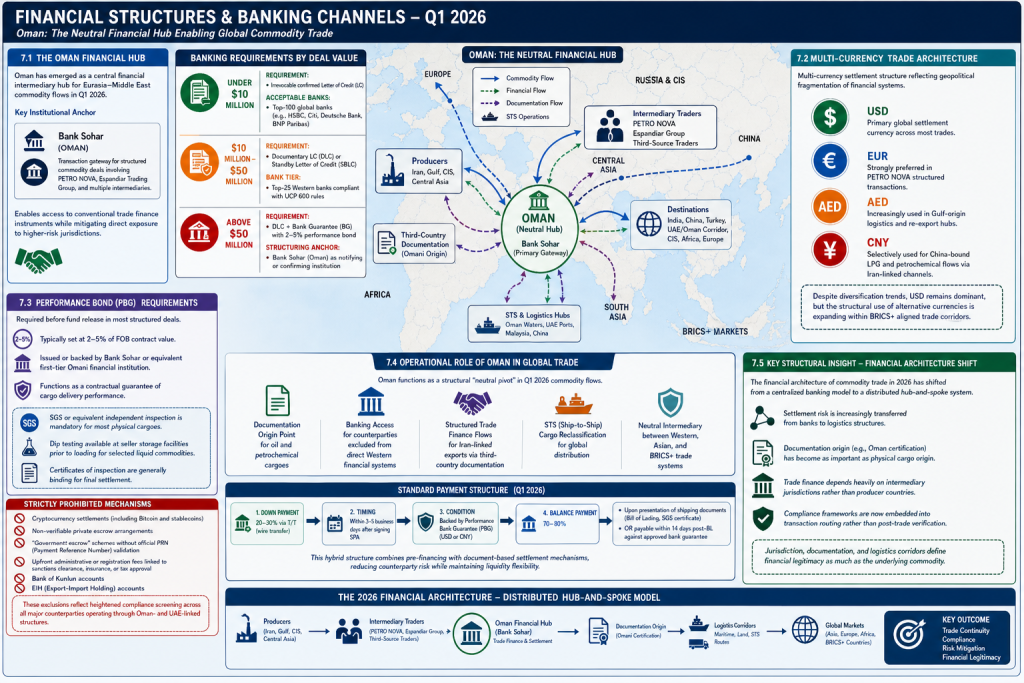

7.1 THE OMAN FINANCIAL HUB

Oman has emerged as a central financial intermediary hub for Eurasia–Middle East commodity flows in Q1 2026. The structure is particularly significant in enabling trade continuity for hydrocarbons, petrochemicals, and fertiliser markets that require neutral jurisdictional settlement mechanisms.

A key institutional anchor in this system is Bank Sohar (Oman), which functions as a transaction gateway for structured commodity deals involving PETRO NOVA, Espandiar Trading Group, and multiple third-source intermediaries.

This structure allows counterparties to access conventional trade finance instruments while mitigating direct exposure to higher-risk jurisdictions.

BANKING REQUIREMENTS BY DEAL VALUE

Trade finance structuring varies depending on transaction size:

- Transactions under $10 million

- Require: Irrevocable confirmed Letter of Credit (LC)

- Acceptable banks: Top-100 global banks (e.g., HSBC, Citi, Deutsche Bank, BNP Paribas)

- Transactions between $10 million and $50 million

- Require: Documentary LC (DLC) or Standby Letter of Credit (SBLC)

- Bank tier: Top-25 Western banks compliant with UCP 600 rules

- Transactions above $50 million

- Require: DLC + Bank Guarantee (BG) with 2–5% performance bond

- Structuring anchor: Bank Sohar (Oman) as notifying or confirming institution

This tiered structure reflects increasing reliance on sovereign-neutral financial intermediaries as transaction size and compliance risk increase.

STANDARD PAYMENT STRUCTURE

Across most structured commodity trades in Q1 2026, a consistent financial pattern is observed:

- Down payment: 20–30% via T/T (wire transfer)

- Timing: within 3–5 business days after signing SPA (Sales and Purchase Agreement)

- Condition: backed by Performance Bank Guarantee (PBG), typically in USD or CNY

- Balance payment: 70–80%

- Released upon presentation of shipping documents (Bill of Lading, SGS certificate)

- Alternatively payable within 14 days post-BL against approved bank guarantee

This hybrid structure combines pre-financing with document-based settlement mechanisms, reducing counterparty risk while maintaining liquidity flexibility.

STRICTLY PROHIBITED MECHANISMS

The following instruments and practices are explicitly excluded from legitimate structured trade flows:

- Cryptocurrency settlements (including Bitcoin and stablecoins)

- Non-verifiable private escrow arrangements

- “Government escrow” schemes without official PRN (Payment Reference Number) validation

- Upfront administrative or registration fees linked to sanctions clearance, insurance, or tax approval

- Bank of Kunlun accounts

- EIH (Export-Import Holding) accounts

These exclusions reflect heightened compliance screening across all major counterparties operating through Oman- and UAE-linked structures.

7.2 MULTI-CURRENCY TRADE ARCHITECTURE

The 2026 commodity trade environment demonstrates a multi-currency settlement structure reflecting geopolitical fragmentation of financial systems.

Key currency preferences:

- USD: Primary global settlement currency across most trades

- EUR: Strongly preferred in PETRO NOVA structured transactions

- AED: Increasingly used in Gulf-origin logistics and re-export hubs

- CNY: Selectively used for China-bound LPG and petrochemical flows via Iran-linked channels

Despite diversification trends, USD remains dominant, but the structural use of alternative currencies is expanding within BRICS+ aligned trade corridors.

7.3 PERFORMANCE BOND (PBG) REQUIREMENTS

Performance Bonds have become a central risk management mechanism in Q1 2026 commodity trade structures.

Key characteristics:

- Required before fund release in most structured deals

- Typically set at 2–5% of FOB contract value

- Issued or backed by Bank Sohar or equivalent first-tier Omani financial institution

- Functions as a contractual guarantee of cargo delivery performance

Additionally:

- SGS or equivalent independent inspection is mandatory for most physical cargoes

- Dip testing is available at seller storage facilities prior to loading for selected liquid commodities

- Certificates of inspection are generally binding for final settlement

This framework reinforces trust in physically delivered commodities while enabling cross-border transactions in fragmented regulatory environments.

7.4 OPERATIONAL ROLE OF OMAN IN GLOBAL TRADE

Oman functions as a structural “neutral pivot” in Q1 2026 commodity flows.

Its role includes:

- Acting as a documentation origin point for oil and petrochemical cargoes

- Providing banking access for counterparties excluded from direct Western financial systems

- Hosting structured trade finance flows for Iran-linked exports routed via third-country documentation

- Supporting STS (ship-to-ship) cargo reclassification for global distribution

This positioning allows Oman to operate as a stabilising financial and logistical intermediary between Western, Asian, and BRICS+ trade systems.

7.5 KEY STRUCTURAL INSIGHT — FINANCIAL ARCHITECTURE SHIFT

The financial architecture of commodity trade in 2026 has shifted from a centralized banking model to a distributed hub-and-spoke system.

Core characteristics:

- Settlement risk is increasingly transferred from banks to logistics structures

- Documentation origin (e.g., Oman certification) has become as important as physical cargo origin

- Trade finance depends heavily on intermediary jurisdictions rather than producer countries

- Compliance frameworks are now embedded into transaction routing rather than post-trade verification

This marks a structural evolution in global commodity finance where jurisdiction, documentation, and logistics corridors define financial legitimacy as much as the underlying commodity itself.

WEALDRAED THRYMMELLEN

Email: info@wealdraedthrymmellen.org

Phone: +971 58 540 3888

Downloadable link: https://drive.google.com/uc?export=download&id=16huleqgxU2FkY8RIyn-J50JVIdUAXGvs

Report Period: January – April 2026

Published: May 2026

Sources: S&P Global Platts · Argus Media · LME · CBOT · Baltic Exchange · EIA · IEA · USDA · World Bank · LBMA · OPEC · FAO · ISCC · wealdraedthrymmellen.org