PART 6 — SUPPLIER PROFILES & COMMERCIAL INTELLIGENCE: Q1 2026 GLOBAL COMMODITY MARKETS

WEALDRAED THRYMMELLEN

Email: info@wealdraedthrymmellen.org

Phone: +971 58 540 3888

Downloadable link: https://drive.google.com/uc?export=download&id=16huleqgxU2FkY8RIyn-J50JVIdUAXGvs

Report Period: January – April 2026

Published: May 2026

Sources: S&P Global Platts · Argus Media · LME · CBOT · Baltic Exchange · EIA · IEA · USDA · World Bank · LBMA · OPEC · FAO · ISCC · wealdraedthrymmellen.org

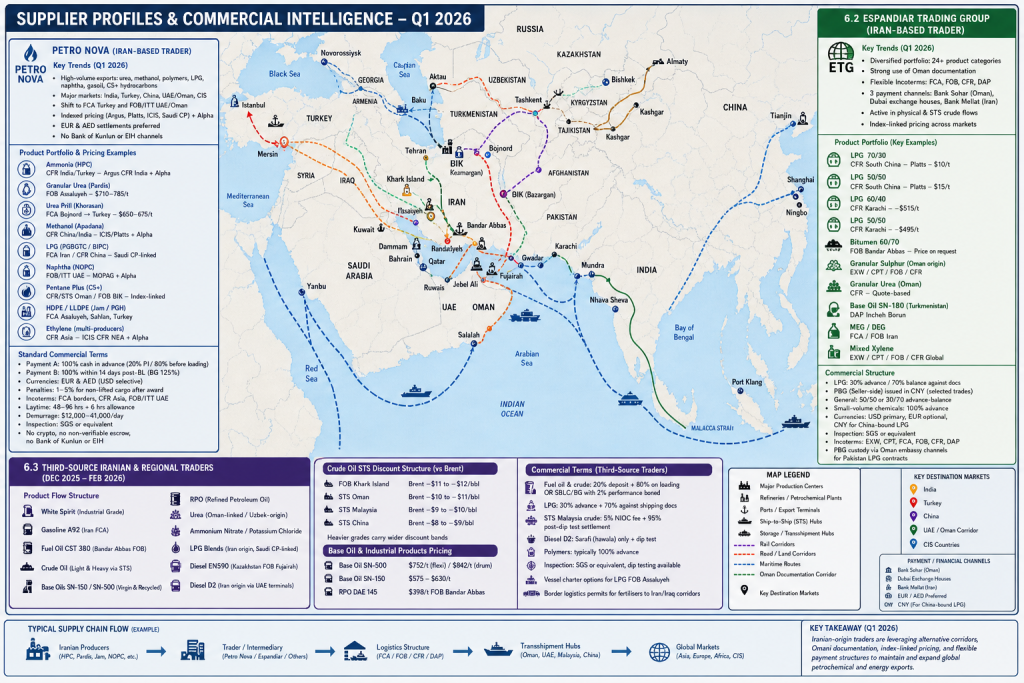

6.1 PETRO NOVA (IRAN-BASED TRADER)

Report period: April 2026 (reflecting Q1 activity and forward offers)

PETRO NOVA operates as a commercial intermediary facilitating export flows from major Iranian petrochemical and refining producers. These include HPC, Pardis, Jam, Kermanshah, NOPC, BIPC, and Apadana.

KEY OBSERVABLE TRENDS

The following structural patterns define PETRO NOVA’s Q1 2026 commercial activity:

- High-volume continuous exports of petrochemicals and energy products including urea, methanol, polymers, LPG, naphtha, gasoil, and light hydrocarbons (C5+)

- Major destination markets include India, Turkey, China, the UAE/Oman corridor, and CIS countries

- Strong operational shift toward FCA Turkey and FOB/ITT UAE/Oman delivery structures

- Reduced reliance on direct Iranian export ports due to compliance and logistics constraints

- Heavy use of indexed pricing systems (Argus, Platts, ICIS, Saudi Aramco CP) combined with an adjustable “Alpha” premium/discount mechanism

- Increased risk allocation to buyers through price variability and index-linked contracts

- Explicit exclusion of Bank of Kunlun and EIH financial channels

- Preference for EUR and AED settlements over USD in selected flows

- Strong reliance on short-cycle tenders, particularly for methanol, urea, and naphtha allocations

PETRO NOVA PRODUCT PORTFOLIO

Product flows are structured across multiple producers and destinations:

- Ammonia (HPC): CFR India/Turkey, Argus CFR India + Alpha pricing

- Granular Urea (Pardis): FOB Assaluyeh, auction-based or fixed pricing ($710–785/t)

- Granular Urea (Kermanshah): FOB BIK / FCA Kermanshah ($770–785/t)

- Urea Prill (Khorasan): FCA Bojnord → Turkey ($650–675/t)

- Methanol (Apadana): CFR China/India (ICIS/Platts + Alpha adjustment)

- LPG (PGBGTC / BIPC): FCA Iran / CFR China (Saudi CP-linked pricing)

- Naphtha (NOPC): FOB/ITT UAE, MOPAG index + Alpha

- Pentane Plus (C5+): CFR/STS Oman / FOB BIK, index-linked pricing

- HDPE / LLDPE (Jam / Persian Gulf Holding): FCA Asaluyeh, Sahlan, Turkey

- Ethylene (multiple producers): CFR Asia via ICIS CFR NEA + Alpha adjustments

STANDARD COMMERCIAL TERMS (PETRO NOVA)

Financial and contractual structure:

- Payment Option A: 100% cash in advance (typically 20% on proforma invoice, 80% before loading)

- Payment Option B: 100% within 14 days post-BL against acceptable bank guarantee (125% coverage)

- Preferred currencies: EUR and AED (USD accepted selectively)

- Strict penalty clauses: 1–5% penalties for non-lifted cargo after tender award

- Logistics formats: FCA land borders (Turkey, Iraq, Afghanistan, CIS), CFR Asia routes, FOB/ITT UAE structures

- Laytime: 48–96 hours standard, plus 6-hour allowance

- Demurrage: $12,000–41,000 per day depending on vessel and cargo class

- Mandatory inspection: SGS or equivalent pre-shipment certification

- Prohibition: no cryptocurrency, no non-verifiable escrow, no Bank of Kunlun or EIH accounts

6.2 ESPANDIAR TRADING GROUP (IRAN-BASED TRADER)

Report period: January–April 2026

Espandiar Trading Group operates across diversified petrochemical, fuel, and fertiliser markets with a strong emphasis on regional trade structuring via Oman and intermediary financial channels.

A key development in Q1 2026 is the confirmed ability to execute contracts using Omani documentation structures, enabling trade continuity outside direct Iranian designation.

KEY OBSERVABLE TRENDS

- Highly diversified portfolio spanning over 24 product categories

- Includes crude oil, LPG, methanol, sulphur, bitumen, base oils, solvents, polymers, and glycols

- Increasing reliance on Oman-based contract structuring

- Strong logistical flexibility using FCA, FOB, CFR, and DAP combinations

- Three primary payment channels:

- Bank Sohar (Oman corporate accounts)

- Approved Dubai exchange houses

- Direct Iranian banking channels (Bank Mellat)

- Active market participation in both physical and STS crude flows

- Strong use of index-linked pricing models across petrochemicals and LPG markets

ESPANDIAR PRODUCT PORTFOLIO

Key traded commodities:

- LPG 70/30: CFR South China (Platts – $10/t adjustment)

- LPG 50/50: CFR South China (Platts – $15/t adjustment)

- LPG 60/40: CFR Karachi (~$515/t)

- LPG 50/50: CFR Karachi (~$495/t)

- Bitumen 60/70: FOB Bandar Abbas (price on request)

- Granular sulphur: Oman origin, EXW/CPT/FOB/CFR

- Granular urea: Oman, CFR pricing (quote-based)

- Heavy hydrocarbons: Iran, EXW/CPT Afghanistan routes

- Base oil SN-180: Turkmenistan via DAP Incheh Borun

- MEG / DEG: FCA / FOB Iran

- Mixed xylene: EXW/CPT/FOB/CFR global distribution

ESPANDIAR COMMERCIAL STRUCTURE

Standard transaction framework:

- LPG contracts: 30% advance payment, 70% balance against shipping documents

- Seller-side Performance Bank Guarantee (PBG) issued in CNY for certain transactions

- General trade structure: 50/50 or 30/70 advance-balance split

- Small-volume chemical products: 100% advance payment required

- Currency flexibility: USD primary, EUR optional, CNY used for China-bound LPG

- Inspection: SGS or equivalent at loading point (final certificate binding)

- Flexible Incoterms: EXW, CPT, FCA, FOB, CFR, DAP

- PBG custody arrangements for Pakistan LPG contracts managed via diplomatic channels (Oman embassy structure)

6.3 THIRD-SOURCE IRANIAN & REGIONAL TRADERS

Report period: December 2025 – February 2026

Multiple independent Iranian-linked trading channels demonstrate fragmented but active participation in regional energy and petrochemical flows.

PRODUCT FLOW STRUCTURE

Key traded commodities include:

- White spirit (industrial grade)

- Gasoline A92 (Iran FCA factory origin)

- Fuel oil CST 380 (Bandar Abbas FOB)

- Crude oil (light and heavy grades via STS routing)

- Base oils SN-150 and SN-500 (virgin and recycled grades)

- RPO (refined petroleum oil derivatives)

- Urea (Oman-linked and Uzbek-origin blends)

- Ammonium nitrate and potassium chloride (Central Asian origin)

- LPG blends (Iran origin with Saudi CP linkage)

- Diesel EN590 (Kazakhstan origin FOB Fujairah)

- Diesel D2 (Iran origin via UAE intermediary terminals)

CRUDE OIL STS DISCOUNT STRUCTURE

Ship-to-ship pricing reflects location-based risk and logistics premiums:

- FOB Khark Island: Brent –$11 to –$12/bbl

- STS Oman: Brent –$10 to –$11/bbl

- STS Malaysia: Brent –$9 to –$10/bbl

- STS China: Brent –$8 to –$9/bbl

Heavier crude grades carry slightly wider discount bands due to processing and transport constraints.

BASE OIL AND INDUSTRIAL PRODUCTS

Pricing structure:

- Base oil SN-500: $752/t (flexi), $842/t (drum packaging)

- Base oil SN-150: $575–630/t depending on grade and destination

- RPO DAE 145: $398/t FOB Bandar Abbas

These flows highlight active regional arbitrage between Iranian production, Central Asian feedstocks, and Gulf transshipment hubs.

COMMERCIAL TERMS (THIRD-SOURCE TRADERS)

Financial structure includes:

- Fuel oil and crude: 20% deposit + 80% upon vessel loading OR SBLC/BG structures with 2% performance bond

- LPG: 30% advance + 70% against shipping documentation

- STS Malaysia crude: 5% NIOC contract fee + 95% post-dip test settlement

- Diesel D2: sarafi (hawala) payment only, with mandatory dip testing prior to loading

- Polymers: typically 100% advance or negotiated structured payment

- Inspection: SGS or equivalent mandatory, dip testing available at storage tanks

- Vessel charter options available for LPG FOB Assaluyeh buyers

- Border logistics permits included for Central Asian fertilisers entering Iran/Iraq corridors

WEALDRAED THRYMMELLEN

Email: info@wealdraedthrymmellen.org

Phone: +971 58 540 3888

Downloadable link: https://drive.google.com/uc?export=download&id=16huleqgxU2FkY8RIyn-J50JVIdUAXGvs

Report Period: January – April 2026

Published: May 2026

Sources: S&P Global Platts · Argus Media · LME · CBOT · Baltic Exchange · EIA · IEA · USDA · World Bank · LBMA · OPEC · FAO · ISCC · wealdraedthrymmellen.org