PART 11 — Q2 2026 OUTLOOK & KEY WATCH INDICATORS

WEALDRAED THRYMMELLEN

Email: info@wealdraedthrymmellen.org

Phone: +971 58 540 3888

Downloadable link: https://drive.google.com/uc?export=download&id=16huleqgxU2FkY8RIyn-J50JVIdUAXGvs

Report Period: January – April 2026

Published: May 2026

Sources: S&P Global Platts · Argus Media · LME · CBOT · Baltic Exchange · EIA · IEA · USDA · World Bank · LBMA · OPEC · FAO · ISCC · wealdraedthrymmellen.org

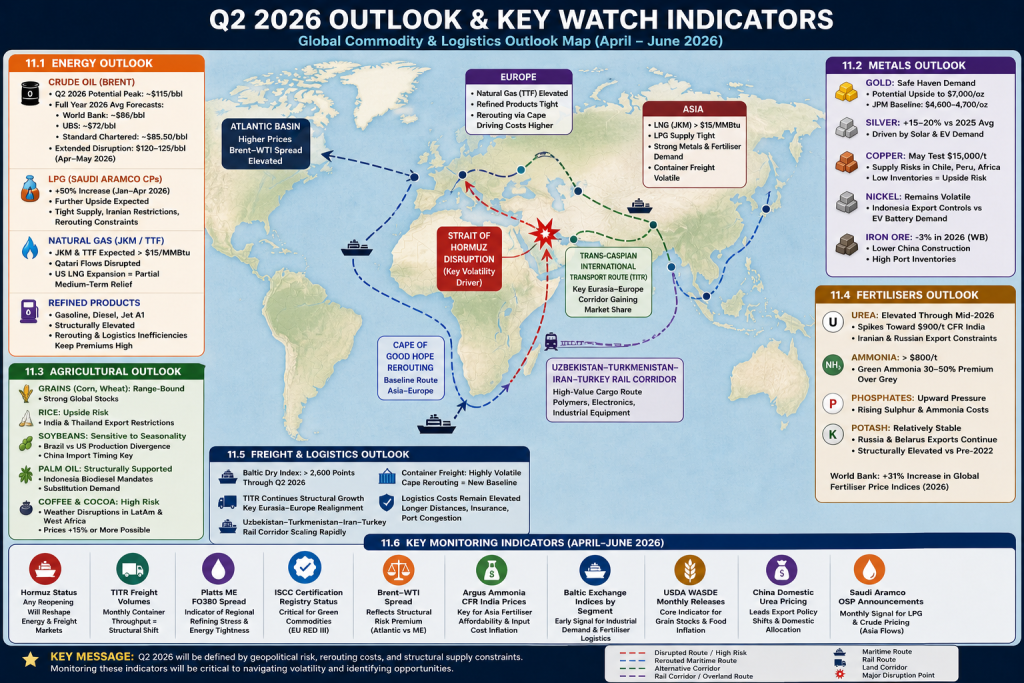

11.1 ENERGY OUTLOOK

Brent crude remains the central volatility driver for Q2 2026. In the event that the Strait of Hormuz remains disrupted, EIA models indicate a potential peak around $115/bbl during Q2. The World Bank baseline scenario assumes a full-year average of approximately $86/bbl for 2026, contingent on conflict stabilisation by mid-year. UBS maintains a lower structural forecast of $72/bbl, while Standard Chartered projects around $85.50/bbl. In extended disruption scenarios, Brent could temporarily test $120–125/bbl during April–May 2026.

LPG markets are expected to remain structurally tight. Saudi Aramco Contract Prices (CPs) have already increased by approximately 50% over a three-month period ending April 2026, and further upward pressure is expected due to restricted Iranian supply and rerouting constraints across the Gulf.

In natural gas markets, JKM (Asia LNG benchmark) and TTF (Europe) are expected to remain elevated above $15/MMBtu through most of Q2 2026. The collapse of Qatari flows via disrupted Gulf routes has tightened supply conditions. However, new US LNG export capacity is expected to provide partial medium-term stabilisation.

Refined products including gasoline, diesel, and jet fuel (Jet A1) are expected to remain structurally elevated across both European and Asian markets due to persistent logistics inefficiencies and rerouting costs via longer maritime corridors.

11.2 METALS OUTLOOK

Gold is expected to remain the primary safe-haven asset through Q2 2026. Some market scenarios suggest potential upside toward $7,000/oz in the event of prolonged geopolitical instability into H2 2026. However, JPMorgan’s baseline full-year forecast places the average in the $4,600–$4,700/oz range, indicating sustained but stabilising elevated pricing.

Silver is forecast by JPMorgan to increase by approximately 15–20% relative to 2025 averages. Structural demand is supported by photovoltaic solar deployment and electric vehicle industrial usage, in addition to macro risk hedging flows.

Copper markets may test the $15,000/t level if supply disruptions persist across Chile, Peru, and African production zones. LME inventories remain historically low, reinforcing upside price sensitivity. The World Bank projects a +17% increase in global metals and minerals indices for 2026.

Nickel markets are expected to remain volatile due to competing forces: Indonesian export controls versus increasing electric vehicle battery demand. Price instability is expected to persist through Q2.

Iron ore is projected by the World Bank to decline approximately 3% in 2026 overall, driven by reduced Chinese construction demand and elevated port inventories, despite short-term volatility spikes.

11.3 AGRICULTURAL OUTLOOK

Global grain markets remain fundamentally oversupplied despite energy-driven inflationary pressures.

Corn and wheat prices are expected to remain relatively range-bound due to strong global stocks. However, rice markets present upside risk due to export restrictions in India and Thailand, which could tighten regional supply balances.

Soybean markets are expected to remain sensitive to seasonal divergence between Brazilian and US production cycles, with volatility linked to Chinese import timing.

Palm oil is expected to remain structurally supported due to Indonesia’s biodiesel blending mandates and substitution demand from competing vegetable oils.

Cocoa and coffee markets remain highly exposed to climate-driven supply disruptions in West Africa and Latin America. Price increases of 15% or more remain possible if adverse weather conditions persist.

11.4 FERTILISERS OUTLOOK

Urea remains the most structurally disrupted fertiliser market globally. Prices are expected to remain elevated through mid-2026, with potential spikes toward $900/t CFR India in Q2 due to constrained Iranian exports and continued Russian export limitations.

Ammonia markets are expected to remain above $800/t, with green ammonia maintaining a 30–50% premium over conventional grey ammonia.

Phosphate fertilisers are expected to experience sustained upward pressure due to rising sulphur and ammonia input costs, which feed directly into production economics.

Potash markets remain comparatively stable due to continued exports from Russia and Belarus, although pricing remains structurally elevated compared to pre-2022 levels.

The World Bank projects a +31% increase in global fertiliser price indices for full-year 2026, reflecting systemic supply chain constraints rather than demand expansion.

11.5 FREIGHT & LOGISTICS OUTLOOK

Baltic Dry Index levels are expected to remain elevated above 2,600 points through Q2 2026, reflecting sustained demand for bulk commodities and rerouted shipping flows.

The Trans-Caspian International Transport Route (TITR) continues to gain structural market share, serving as a key indicator of long-term Eurasia–Europe logistics realignment.

The Uzbekistan–Turkmenistan–Iran–Turkey rail corridor is expected to scale rapidly, becoming a critical high-value cargo route for polymers, electronics, and industrial equipment.

Container freight markets are expected to remain highly volatile, with Cape of Good Hope rerouting becoming a baseline assumption for Asia–Europe trade flows involving Gulf exposure.

Overall logistics costs are expected to remain structurally elevated due to longer transit distances, increased insurance premiums, and port congestion across alternative corridors.

11.6 KEY MONITORING INDICATORS (APRIL–JUNE 2026)

The following indicators represent the primary variables to monitor during Q2 2026:

- Hormuz Status: Any partial reopening or restoration of commercial transit will materially reshape global energy pricing and freight flows.

- TITR Freight Volumes: Monthly container throughput data will indicate the structural shift of Eurasian trade toward the Middle Corridor.

- Platts ME FO380 Spread: A leading indicator of regional refining stress and energy market tightness.

- ISCC Certification Registry Status: Critical for determining eligibility of green commodities under EU RED III compliance frameworks.

- Brent–WTI Spread: Reflects structural risk premium between Atlantic Basin and Middle Eastern supply systems.

- Argus Ammonia CFR India Spot Prices: Key benchmark for Asian fertiliser affordability and agricultural input cost inflation.

- Baltic Exchange Indices by Segment: Capesize and Supramax trends provide early signals for industrial demand and fertiliser logistics.

- USDA WASDE Monthly Releases: Core indicator for global grain stock trajectory and food inflation expectations.

- China Domestic Urea Pricing: Leading indicator of export policy shifts and domestic fertiliser allocation dynamics.

- Saudi Aramco OSP Announcements: Monthly signal for LPG and crude pricing direction across Asia-bound flows.

WEALDRAED THRYMMELLEN

Email: info@wealdraedthrymmellen.org

Phone: +971 58 540 3888

Downloadable link: https://drive.google.com/uc?export=download&id=16huleqgxU2FkY8RIyn-J50JVIdUAXGvs

Report Period: January – April 2026

Published: May 2026

Sources: S&P Global Platts · Argus Media · LME · CBOT · Baltic Exchange · EIA · IEA · USDA · World Bank · LBMA · OPEC · FAO · ISCC · wealdraedthrymmellen.org