PART 1 Petroleum, Gaz, Coal: Q1 2026 GLOBAL COMMODITY MARKETS

Strategic Analysis & New Logistics Realities

WEALDRAED THRYMMELLEN

Email: info@wealdraedthrymmellen.org

Phone: +971 58 540 3888

Downloadable link: https://drive.google.com/uc?export=download&id=16huleqgxU2FkY8RIyn-J50JVIdUAXGvs

Report Period: January – April 2026

Published: May 2026

Sources: S&P Global Platts · Argus Media · LME · CBOT · Baltic Exchange · EIA · IEA · USDA · World Bank · LBMA · OPEC · FAO · ISCC · wealdraedthrymmellen.org

EXECUTIVE SUMMARY

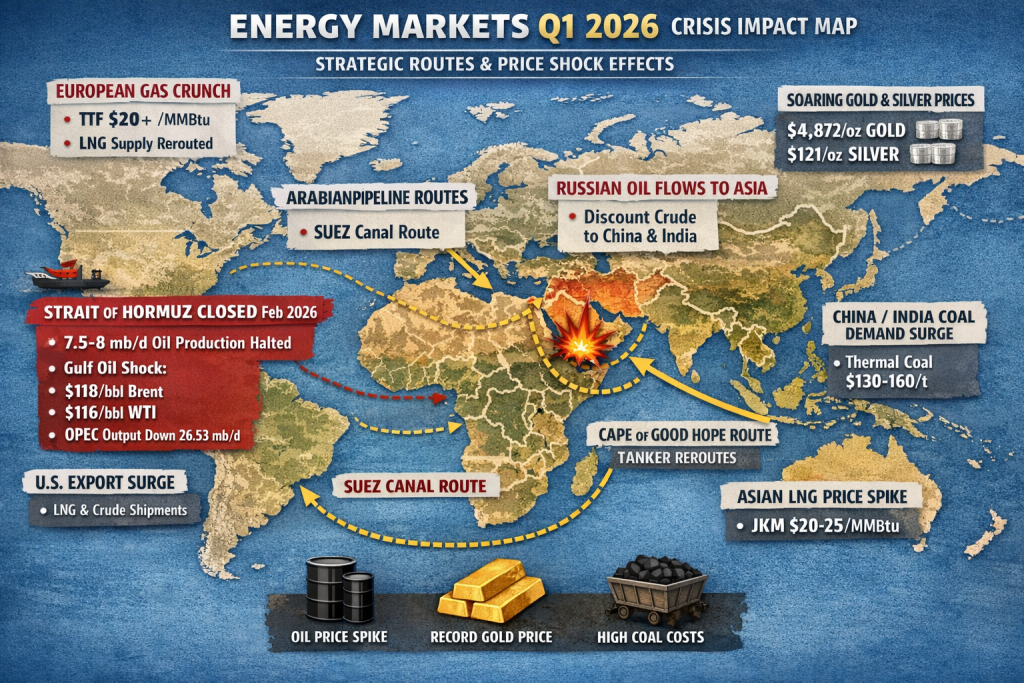

Q1 2026 was defined by a single seismic event: the effective closure of the Strait of Hormuz following military escalation on 28 February 2026. This triggered the largest quarterly oil price surge in inflation-adjusted terms since 1988, drove a global scramble for alternative logistics corridors, and unleashed cascading inflationary pressure across energy, fertilisers, metals, and agriculture. The following consolidated report synthesises all available market intelligence across supplier profiles, pricing data, logistics developments, geopolitical analysis, and financial structures.

KEY INDICATORS

Indicator: Brent Crude (front-month)

Q1 2026 Value: $61 → $118/bbl

Change: +93%

Source: EIA / S&P Global Platts

Indicator: WTI (NYMEX)

Q1 2026 Value: $58 → $116/bbl

Change: +100%

Source: EIA

Indicator: Gold (LBMA PM fix avg)

Q1 2026 Value: $4,872.90/oz (record)

Change: +74% YoY value

Source: LBMA / WGC

Indicator: Silver (LBMA)

Q1 2026 Value: Peak $121.67/oz (record)

Change: +150% since 2025

Source: LBMA

Indicator: Copper (LME 3-month)

Q1 2026 Value: Peak $14,527.50/t (record)

Change: LME index +30.5% in 2025

Source: LME

Indicator: Granular Urea FOB Middle East

Q1 2026 Value: $710–785/t

Change: +75–90% Q1

Source: Argus / PETRO NOVA

Indicator: Baltic Dry Index (avg)

Q1 2026 Value: ~1,956.6 pts

Change: +32% YoY

Source: Baltic Exchange

Indicator: LPG Propane CP (Jan)

Q1 2026 Value: $525/t

Change: +30 vs Dec

Source: Saudi Aramco / Argus

Indicator: World Bank Commodity Index

Q1 2026 Value: +16% forecast 2026

Change: First rise since 2022

Source: World Bank

Indicator: Fertiliser price index

Q1 2026 Value: +31% forecast 2026

Source: World Bank

PART 1 — ENERGY MARKETS

1.1 Crude Oil — Historic Quarterly Surge

The oil market recorded its strongest quarterly rise in inflation-adjusted dollars since 1988. Brent moved from approximately $61/bbl in January to a peak of $118/bbl on 9 March 2026 (+93%), while WTI reached $116/bbl (+100%). The Brent-WTI spread widened to $25/bbl in March — its highest in five years — reflecting insurance surcharges and rerouting costs as US stocks remained relatively insulated.

Period: January 2026

Brent ($/bbl): ~61

WTI ($/bbl): ~58

Key Event: Market opens with geopolitical tension building

Period: February 2026

Brent ($/bbl): ~70

WTI ($/bbl): ~67

Key Event: Escalation begins; insurance premiums rise

Period: 9 March 2026

Brent ($/bbl): 118 (peak)

WTI ($/bbl): 116 (peak)

Key Event: Strait of Hormuz effectively closed

Q1 Average (Platts spot): 80.60

Q2 2026 EIA forecast: ~115 (peak)

Full-year 2026 EIA forecast: ~96 avg

The production disruption was severe: EIA estimated 7.5–8.0 million barrels per day of crude production halted in March. OPEC output fell to 26.53 mb/d in January. Saudi Arabia's quota was fixed at 10.103 mb/d, while its Official Selling Price (OSP) to Asia initially moderated to maintain market share (+0.30 $/bbl over Oman/Dubai), then surged to a record premium of $19.50/bbl in April reflecting acute supply stress.

1.2 Natural Gas

US Henry Hub prices ranged between $3.10 and $4.40/MMBtu in Q1; EIA initially forecast $4.35 but revised to ~$3.50/MMBtu. European TTF remained elevated on supply disruption fears. The Henry Hub–TTF spread narrowed dramatically to just $0.23/MMBtu (from ~$0.95 in 2024), compressing arbitrage opportunities. JKM (Asian LNG spot) and TTF prices surged to $20.4–$25.4/MMBtu in March, with JKM averaging $17.92/MMBtu in April vs. $15.34 for TTF. Global LNG supply is expected to grow 7%+ in 2026, with over 85% from North America, but the geopolitical shock radically altered short-term dynamics.

1.3 LPG — Saudi Aramco Contract Prices

Month: December 2025

Propane CP ($/t): 495

Butane CP ($/t): 485

Change vs. Prior Month: —

Month: January 2026

Propane CP ($/t): 525

Butane CP ($/t): 520

Change vs. Prior Month: +30 / +35

Month: February 2026

Propane CP ($/t): 545

Butane CP ($/t): 540

Change vs. Prior Month: +20 / +20

Month: March 2026

Propane CP ($/t): 545

Butane CP ($/t): 540

Change vs. Prior Month: Stable

Month: April 2026

Propane CP ($/t): 750

Butane CP ($/t): 800

Change vs. Prior Month: +205 / +260 — near-50% in 3 months

Iranian LPG (50/50 blend) offers from PETRO NOVA (FOB Assaluyeh) were priced at Saudi Aramco CP minus $75/t. CFR China cargoes traded at Platts LPGaswire CFR South China minus $10–15/t. Espandiar's CFR Karachi offers ranged from $495–515/t depending on blend.

1.4 Refined Products

Product: Diesel EN590

Grade/Origin: 10ppm – Kazakhstan

Price: $595/t

Delivery Term: FOB Fujairah

Payment: Dip & pay

Product: Diesel D2

Grade/Origin: 5,000ppm – Iran

Price: $585+5/t

Delivery Term: IPL Hamriyeh (UAE)

Payment: Hawala (sarafi) only

Product: Fuel Oil CST 380

Origin: Iran / Bandar Abbas

Price: Platts ME FO380 – $20/t

Delivery: FOB Bandar Abbas

Payment: 20% exchange deposit + 80% on loading

Product: Gasoline A92

Origin: Iran

Price: $795/t

Delivery: FCA Factory

Payment: Negotiated

Product: White Spirit

Origin: Iran

Price: $680/t

Delivery: FCA Factory

Payment: Negotiated

1.5 Iranian Crude — STS Discount Ladder

Transfer Point: FOB Khark Island (Iran)

Discount to Brent: Brent – $11–12/bbl (light/heavy)

Transfer Point: STS Oman

Discount to Brent: Brent – $10–11/bbl

Transfer Point: STS Malaysia

Discount to Brent: Brent – $9–10/bbl

Transfer Point: STS China

Discount to Brent: Brent – $8–9/bbl

1.6 Coal

Australian thermal coal fluctuated between $130–160/t for near-dated contracts, driven by maritime supply disruption fears. Asian demand (India, China, ASEAN) remained robust. European demand continued its structural decline. Chinese domestic coal prices were pressured by high stockpiles and mild heating demand.

WEALDRAED THRYMMELLEN

Email: info@wealdraedthrymmellen.org

Phone: +971 58 540 3888

Downloadable link: https://drive.google.com/uc?export=download&id=16huleqgxU2FkY8RIyn-J50JVIdUAXGvs