KZ-EU NEW RULES

THE KAZAKHSTAN–EUROPE ENERGY CORRIDOR – 2026 REALITIES

- Published on: wealdraedthrymmellen.org

- Email: info@wealdraedthrymmellen.org

- Phone: +971 58 540 3888

- Topic: Energy logistics, regulatory framework, and market context

- Download link: https://drive.google.com/uc?export=download&id=1K38j_8f_ZISyFsAswAYSHMjj1JsfQKzd

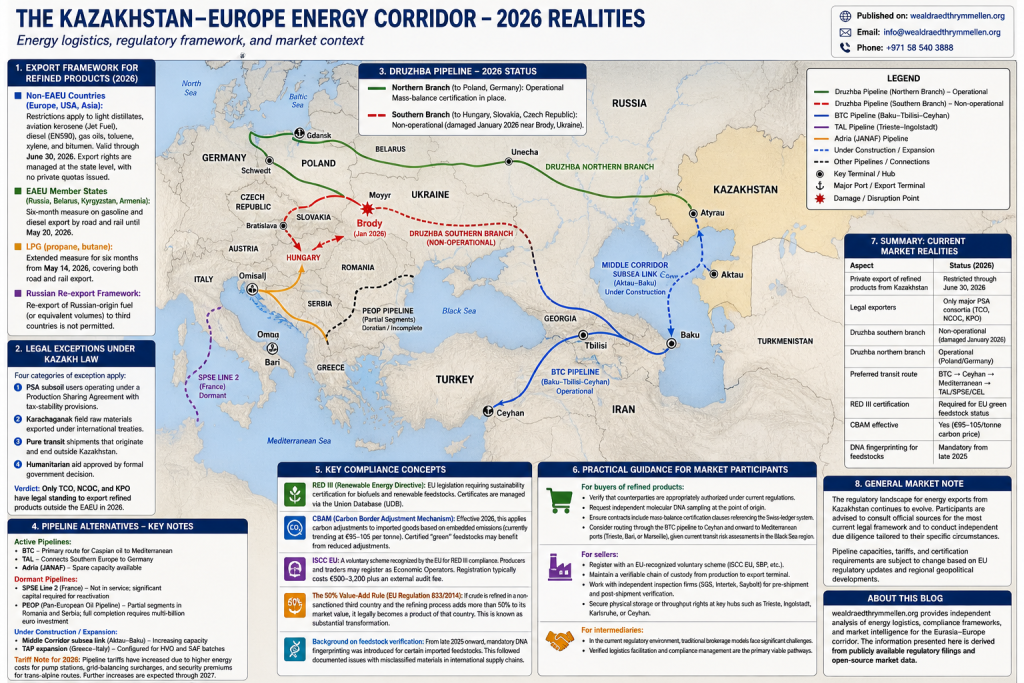

1. THE 2026 EXPORT FRAMEWORK FOR REFINED PRODUCTS

As of early 2026, Kazakhstan has extended export restrictions on certain refined petroleum products.

For non-EAEU countries (Europe, USA, Asia):

Restrictions apply to light distillates, aviation kerosene (Jet Fuel), diesel (EN590), gas oils, toluene, xylene, and bitumen. The current validity period extends through June 30, 2026. Export rights are managed at the state level, with no private quotas issued for 2026.

For EAEU member states (Russia, Belarus, Kyrgyzstan, Armenia):

A six-month measure on gasoline and diesel export by road and rail is in place until May 20, 2026.

For LPG (propane, butane):

An extended measure runs for six months from May 14, 2026, covering both road and rail export.

The Russian Re-export framework:

Kazakhstan imports certain fuel products from Russia under a bilateral arrangement. A condition of this arrangement is that re-export of Russian-origin fuel (or equivalent volumes) to third countries is not permitted.

2. LEGAL EXCEPTIONS UNDER KAZAKH LAW

Under existing regulations, four categories of exception apply:

- PSA subsoil users operating under a Production Sharing Agreement with tax-stability provisions.

- Karachaganak field raw materials exported under international treaties.

- Pure transit shipments that originate and end outside Kazakhstan.

- Humanitarian aid approved by formal government decision.

In practice, the entities currently operating under stabilized contracts include major consortia such as Tengizchevroil (TCO), North Caspian Operating Company (NCOC), and Karachaganak Petroleum Operating (KPO).

Verdict from public information: Only these three major consortia have legal standing to export refined products outside the EAEU in 2026.

3. THE DRUZHBA PIPELINE – 2026 OPERATIONAL STATUS

Southern branch (to Hungary, Slovakia, Czech Republic):

Sustained damage in January 2026 near the Brody hub in Ukraine. Flow has been interrupted since that time, creating supply tensions in the region.

Northern branch (to Poland and Germany):

Remains operational. Crude continues to move to Germany via this route under a mass-balance certification framework.

Mass-balance certification explained:

Because oil must transit infrastructure shared with other sources, a ledger-based system tracks injection and withdrawal volumes. Independent inspectors verify volumes and chemical signatures at the point of entry. This allows certified volumes to be distinguished at the point of delivery.

EU Regulation 2026/261 (effective February 2026):

Non-Russian oil moving through the Druzhba system requires five-day advance notification. Certification is currently recognized only for national-level entities, not private brokers.

4. EUROPEAN PIPELINE ALTERNATIVES

Active pipelines:

BTC Baku → Tbilisi → Ceyhan Primary route for Caspian oil to Mediterranean

TAL Trieste → Ingolstadt Connects Southern Europe to Germany

Adria (JANAF) Croatia → Hungary/Slovakia Spare capacity available

Dormant pipelines:

- SPSE Line 2 (France): Currently not in service. Reactivation would require significant capital investment.

- PEOP (Pan-European Oil Pipeline): Partial segments exist in Romania and Serbia. Full completion would involve multi-billion euro investment.

Under construction or expansion:

- Middle Corridor subsea link (Aktau–Baku): Designed to increase capacity.

- TAP expansion (Greece–Italy): Configured for HVO and SAF batches.

Tariff note for 2026:

Pipeline tariffs have increased due to higher energy costs for pump stations, grid-balancing surcharges, and security premiums for trans-alpine routes. Further increases are expected through 2027.

5. KEY COMPLIANCE CONCEPTS

RED III (Renewable Energy Directive):

EU legislation requiring sustainability certification for biofuels and renewable feedstocks. Certificates are managed via the Union Database (UDB).

CBAM (Carbon Border Adjustment Mechanism):

Effective 2026, this applies carbon adjustments to imported goods based on embedded emissions (currently trending at €95–105 per tonne). Certified "green" feedstocks may benefit from reduced adjustments.

ISCC EU:

A voluntary scheme recognized by the EU for RED III compliance. Producers and traders may register as Economic Operators. Registration typically costs €500–3,200 plus an external audit fee.

The 50% Value-Add Rule (EU Regulation 833/2014):

If crude is refined in a non-sanctioned third country and the refining process adds more than 50% to its market value, it legally becomes a product of that country. This is known as substantial transformation.

Background on feedstock verification:

From late 2025 onward, mandatory DNA fingerprinting was introduced for certain imported feedstocks. This followed documented issues with misclassified materials in international supply chains.

6. PRACTICAL GUIDANCE FOR MARKET PARTICIPANTS

For buyers of refined products:

- Verify that counterparties are appropriately authorized under current regulations.

- Request independent molecular DNA sampling at the point of origin.

- Ensure contracts include mass-balance certification clauses referencing the Swiss-ledger system.

- Consider routing through the BTC pipeline to Ceyhan and onward to Mediterranean ports (Trieste, Bari, or Marseille), given current transit risk assessments in the Black Sea region.

For sellers:

- Register with an EU-recognized voluntary scheme (ISCC EU, SBP, etc.).

- Maintain a verifiable chain of custody from production to export terminal.

- Work with independent inspection firms (SGS, Intertek, Saybolt) for pre-shipment and post-shipment verification.

- Secure physical storage or throughput rights at key hubs such as Trieste, Ingolstadt, Karlsruhe, or Ceyhan.

For intermediaries:

- In the current regulatory environment, traditional brokerage models face significant challenges.

- Verified logistics facilitation and compliance management are the primary viable pathways.

7. SUMMARY: CURRENT MARKET REALITIES

Aspect Status (2026)

Private export of refined products from Kazakhstan Restricted through June 30, 2026

Legal exporters Only major PSA consortia (TCO, NCOC, KPO)

Druzhba southern branch Non-operational (damaged January 2026)

Druzhba northern branch Operational (Poland/Germany)

Preferred transit route BTC → Ceyhan → Mediterranean → TAL/SPSE/CEL

RED III certification Required for EU green feedstock status

CBAM effective Yes (€95–105/tonne carbon price)

DNA fingerprinting for feedstocks Mandatory from late 2025

8. GENERAL MARKET NOTE

The regulatory landscape for energy exports from Kazakhstan continues to evolve. Participants are advised to consult official sources for the most current legal framework and to conduct independent due diligence tailored to their specific circumstances.

Pipeline capacities, tariffs, and certification requirements are subject to change based on EU regulatory updates and regional geopolitical developments.

ABOUT THIS BLOG

wealdraedthrymmellen.org provides independent analysis of energy logistics, compliance frameworks, and market intelligence for the Eurasia–Europe corridor. The information presented here is derived from publicly available regulatory filings and open-source market data.

- Published on: wealdraedthrymmellen.org

- Email: info@wealdraedthrymmellen.org

- Phone: +971 58 540 3888

- Download link: https://drive.google.com/uc?export=download&id=1K38j_8f_ZISyFsAswAYSHMjj1JsfQKzd